The screen glows in the dark of a teenage bedroom. A thumb scrolls. It passes the usual dance trends, the gaming clips, the memes that evaporate from relevance in a matter of hours. Then, a familiar face appears, backed by the unmistakable glitz of a branding empire that has spanned decades. But this time, the pitch isn't directed at voters, real estate moguls, or reality television fans. This time, the call to action is aimed squarely at minors.

The announcement that specialized financial accounts bearing the Trump brand are being launched specifically for kids under eighteen marks a profound shift in how public figures engage with the youth. It bridges the gap between political fandom, digital finance, and the impressionable nature of adolescence. Stripping away the standard corporate press releases reveals a deeper, more complicated reality about what it means to grow up in an era where childhood itself is being monetized by political heavyweights.

Consider a hypothetical teenager named Leo. He is fourteen, loves video games, and has just started earning a small income from cutting lawns in his neighborhood. Like millions of his peers, Leo is eager for independence. He wants his own card, his own digital wallet, his own slice of the adult world. Historically, getting a bank account meant a mundane trip to a brick-and-mortar branch with a parent, signing papers, and receiving a plastic card with a generic logo.

Now, the digital ecosystem offers an entirely different path. By attaching a highly polarizing, deeply charismatic political brand to a financial product aimed at minors, the traditional concept of a youth savings account transforms into an identity statement. It is no longer just about storing money. It becomes about choosing a side before you are even old enough to cast a ballot.

The Mechanics Behind the Glossy Screen

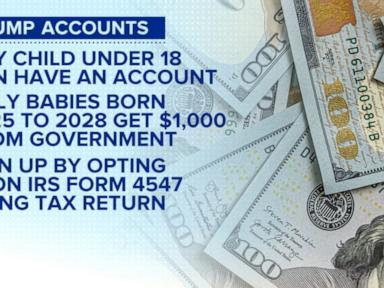

Behind the high-energy promotional videos lies a relatively straightforward financial mechanism, wrapped in sophisticated digital marketing. These new accounts function primarily as digital wallets or debit cards managed through a smartphone app. Because minors cannot legally enter into financial contracts on their own, the accounts require a parent or guardian to co-sign and oversee the activity.

But the marketing is designed to cut straight to the kid.

The promotional material leverages the aesthetics of modern social media: fast cuts, bold text, and promises of exclusive access. Subscribers and account holders are promised perks that appeal directly to a generation raised on internet culture. There are hints of limited-edition merchandise, digital badges, and the psychological thrill of being part of an exclusive club.

The business logic is clear. Capturing a customer early in life is the holy grail of financial institutions. If a brand can secure the loyalty of a fourteen-year-old, there is a strong chance that individual will remain within the ecosystem for decades to come. When that brand is also tied to a massive political movement, the financial tie becomes a cultural anchor.

But the real problem lies elsewhere. Money management is inherently stressful, even for adults. For a teenager, learning how to budget, save, and avoid debt is already a minefield. Introducing the intense emotion of modern political tribalism into a child's first financial tool introduces variables that traditional banks never had to navigate.

When Branding Collides with Financial Literacy

Financial experts have long worried about the gamification of money. Apps that use flashing lights, streaks, and celebratory animations when a user spends or invests money can alter brain chemistry, making financial risk feel like a mobile game. When you layer a political movement on top of that gamified structure, the lines between financial prudence and ideological loyalty blur.

Let's look at how this plays out in real life. Imagine Leo wants to buy a pair of expensive sneakers. In a standard banking app, he might see a simple bar graph showing his savings dwindle. It is a sobering, if boring, reality check. In a highly branded, community-driven ecosystem, however, spending money or participating in specific financial behaviors can be framed as supporting a cause or staying loyal to a movement. The pressure to conform shifts from a peer group at school to a massive, nationwide digital community.

There is a historical precedent for this kind of youth engagement, though rarely has it been tied so directly to personal finance. Political movements have always sought to cultivate the next generation through clubs, youth groups, and educational materials. What makes this move different is the integration of the smartphone. By placing a branded financial tool directly into the pocket of a teenager, the boundary between private life, personal finance, and public ideology dissolves completely.

Parents are left in a difficult position. On one hand, any tool that encourages a teenager to save money and think about their financial future seems like a win. The alternative is often cash hidden under a mattress or unchecked spending on parental credit cards. On the other hand, approving an account means inviting a specific, highly charged political entity into the family's daily financial discussions. Every time a child buys a slice of pizza or saves for a bike, that transaction passes through a filter of political branding.

The Illusion of Early Independence

The desire for autonomy is a defining trait of adolescence. Teenagers want to feel powerful in a world that constantly tells them what to do. Having a card with your name on it provides a tangible sense of adulthood. It feels like freedom.

But true financial independence requires critical thinking, skepticism, and the ability to separate emotion from economic decisions. When a financial product relies heavily on the emotional attachment to a public figure, it teaches the opposite lesson. It suggests that financial choices should be guided by loyalty rather than logic, interest rates, or fee structures.

Consider what happens next when these children turn eighteen. They enter a world of credit card offers, student loans, and complex investment options. If their foundational understanding of banking is rooted in a culture of fandom and identity, they may lack the objective tools needed to evaluate standard financial products. They might choose an account because of the logo on the front rather than the terms and conditions printed on the back.

The digital world has made it incredibly easy to reach children without the traditional gatekeepers of schools, community organizations, or even parental consent in the initial discovery phase. A video on a phone screen bypasses the living room and goes straight to the child's mind. By the time a parent is asked to sign the co-ownership agreement, the teenager is already sold on the concept. The refusal to sign can create a rift, framing the parent not as a financial guide, but as an obstacle to the child's self-expression.

The Evolution of the Pitch

The strategy behind launching these accounts reflects a broader trend in media and commerce. We are moving away from a world where products are sold based on their utility. Instead, everything is sold as an extension of the self. A car is no longer just transportation; it is a statement about your view of the environment. A clothing brand is no longer just fabric; it is an alignment with a specific subculture.

Now, banking is receiving the same treatment for minors.

This approach exploits a vulnerability in the adolescent brain. The prefrontal cortex, which handles long-term planning and risk assessment, is still developing during the teenage years. Meanwhile, the areas of the brain that respond to social rewards, status, and community acceptance are highly active. A financial product that offers status and community recognition is uniquely irresistible to a young mind.

The long-term impact of this experiment remains to be seen. It may result in a generation of highly loyal young investors who feel deeply connected to a specific economic and political vision. Or, it could lead to disillusionment when the realities of fees, restrictions, and the cold logic of banking inevitably clash with the high-energy promises of the marketing campaign.

The screen in the dark bedroom finally goes black. The teenager puts the phone on the nightstand, dreaming of the day the mail carrier arrives with that specific, branded piece of plastic. It is a quiet moment, but one that carries the weight of a changing world, where the contents of a child's wallet are now the front lines of a much larger cultural struggle.