The maritime corridor connecting the Arabian Sea to the Mediterranean has transitioned from a friction point to a permanent risk premium in the global supply chain. While initial discourse focused on the immediate disruption of oil and gas flows, the systemic impact on Asian trade—specifically the non-commodity sectors of manufacturing and intermediate goods—reveals a fundamental breakdown in the "Just-in-Time" logistics model. The crisis in the Gulf and the Red Sea is no longer a temporary detour; it is a catalyst for a structural realignment of how value is moved between East and West.

The logistics of this shift can be quantified through three primary vectors of disruption: the Temporal Gap, the Capacity Siphon, and the Capital Absorption Rate. For a different perspective, read: this related article.

The Temporal Gap: The Erosion of Buffer Stocks

The standard transit from hubs like Shanghai or Singapore to Rotterdam via the Suez Canal typically requires 25 to 30 days. Re-routing vessels around the Cape of Good Hope adds approximately 3,500 to 4,000 nautical miles to the journey, extending transit times by 10 to 14 days. This delay is not a linear inconvenience; it is a compounding operational failure.

In modern lean manufacturing, inventory is viewed as a liability. Most Asian exporters operate on a 14-day buffer for high-value electronic components and automotive parts. The Cape detour effectively exhausts this buffer before the vessel reaches the halfway point. When the lead time exceeds the inventory-on-hand, the result is a "bullwhip effect" where small disruptions at the origin lead to massive stockouts at the destination. The cost of this delay is reflected in the Time-Value of Money (TVM) calculation for cargo: Related reporting regarding this has been provided by MarketWatch.

$$V_{total} = C \cdot (1 + r \cdot \frac{t}{365})$$

Where $C$ is the cargo value, $r$ is the interest rate, and $t$ is the transit time in days. As interest rates remain elevated globally, a 14-day extension on a vessel carrying $200 million in electronics represents a significant unrecovered capital cost for the shipper, even before accounting for fuel or insurance.

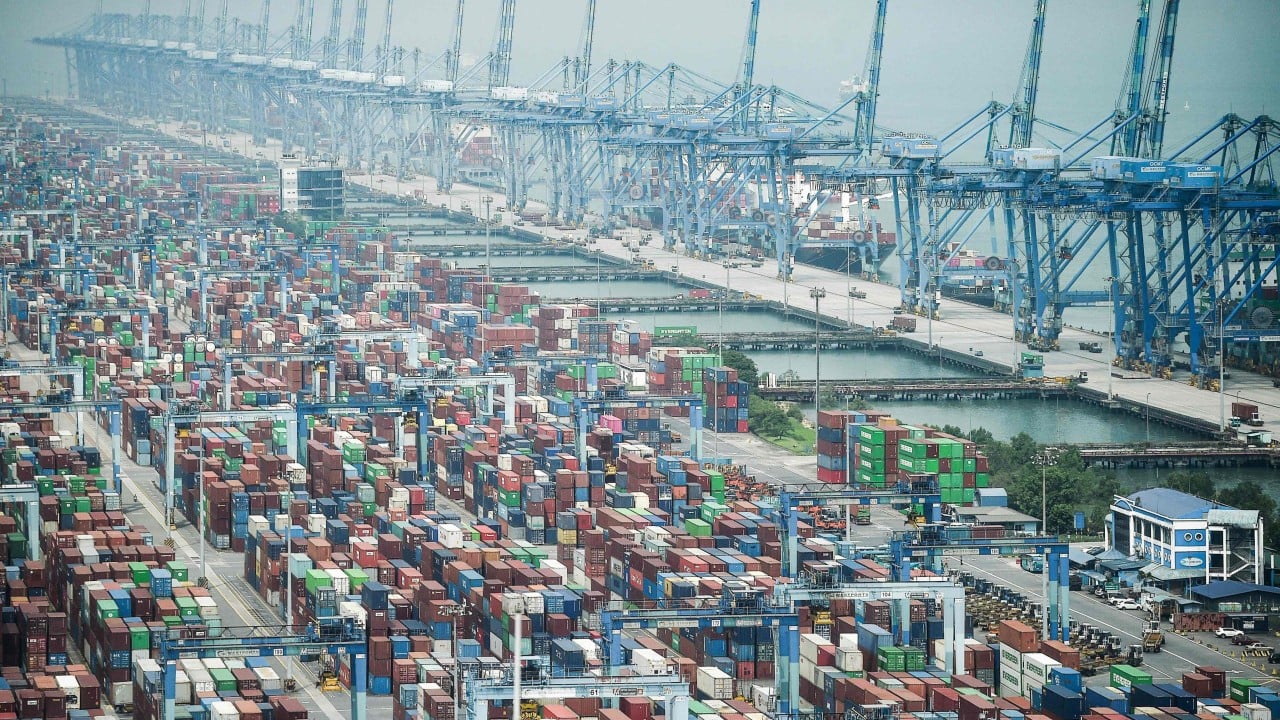

The Capacity Siphon: Artificial Scarcity in a Global Fleet

A common misconception is that delays only affect the specific ships being diverted. In reality, the diversion around Africa creates an artificial contraction of global shipping capacity. If a standard loop between Asia and Europe requires 10 ships to maintain weekly calls, the 25% increase in transit time means that same loop now requires 12 or 13 ships to maintain the same frequency.

The global fleet is finite. With more ships "stuck" on longer routes, the available capacity for other trade lanes—including Trans-Pacific and Intra-Asia—diminishes. This induces a spike in freight rates across the board, not just on the affected routes. We are observing a shift from a Buyer’s Market, characterized by oversupply and low rates, to a Scarcity Model where carriers prioritize high-margin cargo, leaving small-to-medium enterprises (SMEs) in Southeast Asia and South Asia unable to secure space.

The Cost Function of Rerouting: Beyond Bunker Fuel

The financial burden of the Gulf crisis on Asian trade is driven by a complex cost function that involves more than just the price of Brent crude. The total operational expenditure ($OpEx$) for a diverted vessel is defined by:

$$OpEx = F_{b} + I_{w} + L_{c} + E_{u}$$

- $F_{b}$ (Bunker Fuel): Steaming around Africa at higher speeds to minimize the delay increases fuel consumption exponentially. Ship engines follow a cubic power law; doubling the speed requires eight times the power.

- $I_{w}$ (War Risk Insurance): Premiums for transit through the Gulf of Aden have surged, in some cases reaching 1% of the hull value per single voyage. For a modern Ultra Large Container Vessel (ULCV) valued at $200 million, this is a $2 million surcharge per transit.

- $L_{c}$ (Labor and Maintenance): Extended days at sea increase crew costs and accelerate the wear-and-tear on propulsion systems.

- $E_{u}$ (Equipment Utilization): Empty containers are not returning to Asian manufacturing hubs fast enough. This creates a regional shortage of "empties," forcing manufacturers to pay premium "repositioning fees" to get their goods into any available box.

The Industrial Fallout: Sector-Specific Vulnerabilities

The "Asia to the World" trade model is not monolithic. The crisis affects different sectors with varying degrees of severity based on their value-to-weight ratio and the perishability of their demand.

1. Automotive and Heavy Machinery

Japan and South Korea rely on highly synchronized deliveries of sub-assemblies. The delay in Red Sea transits has forced several European assembly plants to pause production. This highlights a critical failure in the "single-source" strategy for specialized components. The inability to pivot to air freight due to the sheer weight of these parts makes this sector the most vulnerable to prolonged maritime instability.

2. Fast-Moving Consumer Goods (FMCG) and Apparel

For retailers in Europe sourcing from Vietnam and Bangladesh, the 14-day delay renders seasonal inventory obsolete. A shipment of spring apparel arriving in early summer must be liquidated at a discount, wiping out the thin margins typically found in these sectors. The result is a shift toward "Near-shoring," with European firms looking to Turkey or Eastern Europe to bypass the maritime choke points entirely.

3. Electronics and High-Tech

While high-value items like semiconductors can be shifted to air freight, the cost differential is staggering. Moving a kilogram of freight by sea costs cents; moving it by air costs dollars. The "Air-Bridge" solution is only sustainable for the top 5% of products by value. For the remaining 95%, the cost of the crisis is being passed directly to the consumer, fueling inflationary pressures in the West and dampened demand for Asian exports.

The Geopolitical Re-balancing: China’s Rail and the Middle Corridor

The disruption of the Suez route has revitalized interest in land-based alternatives. The China-Europe Railway Express (the "Iron Silk Road") has seen a surge in inquiries. However, rail cannot replace the scale of maritime trade. A single ULCV can carry 24,000 TEUs (Twenty-foot Equivalent Units); a train carries roughly 100. It would take 240 trains to replace one ship.

Furthermore, the "Middle Corridor"—a route through Central Asia and the Caucasus—remains plagued by fragmented customs unions and infrastructure bottlenecks. These alternatives are not solutions to the crisis; they are high-cost insurance policies for a small fraction of the total trade volume.

Strategic Infrastructure Limitations

The crisis has exposed the fragility of the "Super-Hub" model. Ports like Singapore and Jebel Ali are designed for high-efficiency throughput. When the schedule of arrivals is disrupted—a phenomenon known as "vessel bunching"—these ports face immediate congestion. Five ships arriving at once instead of one ship per day for five days creates a backlog that can take weeks to clear.

Asian exporters are currently facing a "Double Squeeze." On one side, the cost of production is rising due to energy price volatility linked to the Gulf crisis. On the other, the cost of distribution is inflating due to the maritime detour. This reduces the Global Competitiveness Index of Asian manufacturing hubs relative to those in Mexico (serving the US) or Morocco (serving Europe).

Probability of Permanent Shift: The New Logistics Baseline

Historical data suggests that once supply chains adapt to a higher cost environment, they rarely revert to the previous baseline even if the original disruption is resolved. Carriers have discovered that they can maintain higher freight rates by managing "blank sailings" (canceled trips) and capacity more aggressively.

Exporters must now calculate their Risk-Adjusted Landed Cost. This metric must incorporate the probability of maritime choke point closures. For a firm in Vietnam, the equation is no longer just "Production + Shipping," but:

$$Landed Cost = P + S + (P_{disruption} \times C_{alternative})$$

Where $P_{disruption}$ is the probability of a route closure and $C_{alternative}$ is the cost of emergency air freight or rail.

Operational Mandate for Asian Trade Entities

To navigate this realignment, Asian trade strategy must pivot from cost-optimization to resilience-optimization. This involves three immediate tactical shifts:

- Dynamic Inventory Buffering: Abandoning "Just-in-Time" in favor of "Just-in-Case." This requires increasing regional warehousing capacity at the point of origin to decouple production schedules from shipping schedules.

- Multimodal Diversification: Establishing pre-negotiated contracts for rail and air freight before a crisis hits. Waiting for a disruption to negotiate spot rates is a recipe for margin depletion.

- Digital Twin Simulation: Utilizing real-time data to model the impact of various choke point closures. If the Strait of Malacca or the Panama Canal were to face simultaneous disruptions, few Asian firms have the contingency plans to survive the resulting liquidity crunch.

The Gulf crisis is not a temporary hurdle for Asian trade; it is the definitive end of the era of cheap, predictable maritime logistics. Firms that continue to wait for a "return to normal" will find themselves structurally uncompetitive in a market that has already moved on. The focus must shift to the radical redesign of the supply chain architecture to thrive in a permanent state of volatility.